Impact Cost

Introduction

Liquidity in the context of stock markets means a market where large orders can be executed without incurring a high transaction cost. The transaction cost referred here is not the fixed costs typically incurred like brokerage, transaction charges, depository charges etc. but is the cost attributable to lack of market liquidity as explained subsequently. Liquidity comes from the buyers and sellers in the market, who are constantly on the look out for buying and selling opportunities. Lack of liquidity translates into a high cost for buyers and sellers.

The electronic limit order book (ELOB) as available on NSE is an ideal provider of market liquidity. This style of market dispenses with market makers, and allows anyone in the market to execute orders against the best available counter orders. The market may thus be thought of as possessing liquidity in terms of outstanding orders lying on the buy and sell side of the order book, which represent the intention to buy or sell.

When a buyer or seller approaches the market with an intention to buy a particular stock, he can execute his buy order in the stock against such sell orders, which are already lying in the order book, and vice versa.

An example of an order book for a stock at a point in time is detailed below:

| Buy | Sell | ||||

|---|---|---|---|---|---|

| Sr.No. | Quantity | Price | Quantity | Price | Sr. No. |

| 1 | 1000 | 3.50 | 2000 | 4.00 | 5 |

| 2 | 1000 | 3.40 | 1000 | 4.05 | 6 |

| 3 | 2000 | 3.40 | 500 | 4.20 | 7 |

| 4 | 1000 | 3.30 | 100 | 4.25 | 8 |

There are four buy and four sell orders lying in the order book. The difference between the best buy and the best sell orders (in this case, ₹ 0.50) is the bid-ask spread. If a person places an order to buy 100 shares, it would be matched against the best available sell order at ₹ 4 i.e. he would buy 100 shares for ₹ 4. If he places a sell order for 100 shares, it would be matched against the best available buy order at ₹ 3.50 i.e. the shares would be sold at ₹ 3.5.

Hence if a person buys 100 shares and sells them immediately, he is poorer by the bid-ask spread. This spread may be regarded as the transaction cost which the market charges for the privilege of trading (for a transaction size of 100 shares).

Progressing further, it may be observed that the bid-ask spread as specified above is valid for an order size of 100 shares upto 1000 shares. However for a larger order size the transaction cost would be quite different from the bid-ask spread.

Suppose a person wants to buy and then sell 3000 shares. The sell order will hit the following buy orders:

| Sr. No. | Quantity | Price |

|---|---|---|

| 1 | 1000 | 3.50 |

| 2 | 1000 | 3.40 |

| 3 | 1000 | 3.40 |

while the buy order will hit the following sell orders:

| Sr. No. | Quantity | Price |

|---|---|---|

| 5 | 2000 | 4.00 |

| 6 | 1000 | 4.05 |

This implies an increased transaction cost for an order size of 3000 shares in comparison to the impact cost for order for 100 shares. The "bid-ask spread" therefore conveys transaction cost for a small trade.

This brings us to the concept of impact cost. We start by defining the ideal price as the average of the best bid and offer price, in the above example it is (3.5+4)/2, i.e. 3.75. In an infinitely liquid market, it would be possible to execute large transactions on both buy and sell at prices which are very close to the ideal price of ₹ 3.75. In reality, more than ₹ 3.75 per share may be paid while buying and less than ₹ 3.75 per share may be received while selling. Such percentage degradation that is experienced vis-à-vis the ideal price, when shares are bought or sold, is called impact cost. Impact cost varies with transaction size.

For example, in the above order book, a sell order for 4000 shares will be executed as follows:

| Sr. No. | Quantity | Price | Value |

|---|---|---|---|

| 1 | 1000 | 3.50 | 3500 |

| 2 | 1000 | 3.40 | 3400 |

| 3 | 2000 | 3.40 | 6800 |

| Total value | 13700 | ||

| Wt. average price | 3.43 | ||

The sale price for 4000 shares is ₹ 3.43, which is 8.53% worse than the ideal price of ₹ 3.75. Hence we say "The impact cost faced in buying 4000 shares is 8.53%".

Definition

Impact cost represents the cost of executing a transaction in a given stock, for a specific predefined order size, at any given point of time.

Impact cost is a practical and realistic measure of market liquidity; it is closer to the true cost of execution faced by a trader in comparison to the bid-ask spread.

It should however be emphasised that:

- impact cost is separately computed for buy and sell

- impact cost may vary for different transaction sizes

- impact cost is dynamic and depends on the outstanding orders

- where a stock is not sufficiently liquid, a penal impact cost is applied

In mathematical terms it is the percentage mark up observed while buying / selling the desired quantity of a stock with reference to its ideal price (best buy + best sell) / 2.

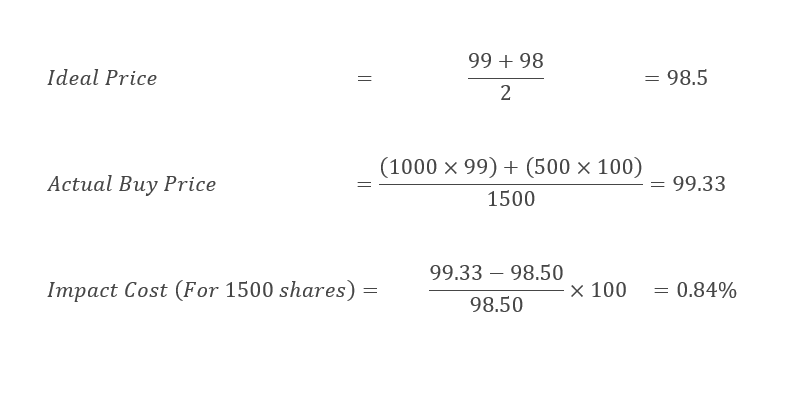

Example A:

| ORDER BOOK SNAPSHOT | |||

|---|---|---|---|

| Buy Quantity | Buy Price | Sell Quantity | Sell Price |

| 1000 | 98 | 1000 | 99 |

| 2000 | 97 | 1500 | 100 |

| 1000 | 96 | 1000 | 101 |

To buy 1500 Shares

Updated on: 06/01/2023